Battery Anode Market

A lithium-ion battery is comprised of four key components: anode, cathode, separator, and electrolyte.

Graphite has historically been and is expected to remain the dominant active material in the anode of the lithium-ion battery, and accounts for the largest proportion of active material in a lithium-ion battery by mass.

Natural graphite active anode materials are expected to account for an increasing proportion of battery anodes supply compared to synthetic graphite, silicon and other additives due to:

Cost competitiveness at scale.

Significantly lower global warming potential (greenhouse gas emissions intensity).

Desirable properties for battery performance.

Balama’s natural graphite product characteristics are ideally suited to the battery anode market, evidenced by the strong customer demand for Balama fine flake graphite, and the development of Vidalia active anode material products.

Lithium-ion is the incumbent battery technology used in most electric vehicles, retail energy storage and consumer electronics applications.

As the world transitions towards an electrified future, and demand increases for batteries, resilient and sustainable supply of battery materials has become a major priority for supply chain participants and governments.

Diversification is Required in Anode Material Supply

The battery anode supply chain is highly dependent on processing facilities in China, Japan and South Korea, with China producing almost all of natural graphite-based anode precursor material (purified spherical graphite). Active anode material is not homogenous. This material requires a high level of processing expertise and extensive qualification processes with customers prior to commercial arrangements and consumption in battery cell manufacturing. The full qualification process for active anode material can take as long as two years.

What is Driving Demand?

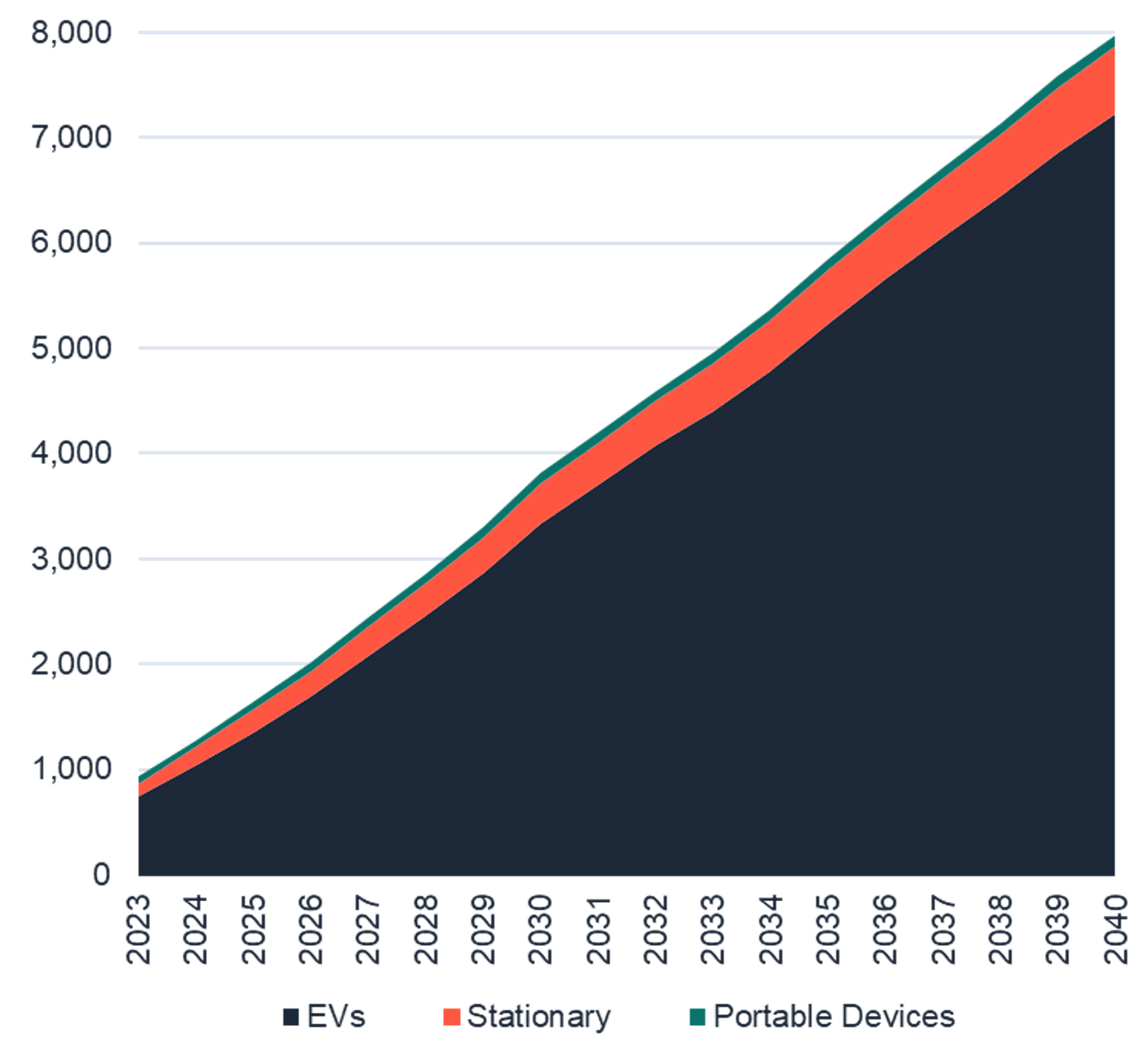

The most significant driver of lithium-ion battery and active anode material demand is the global adoption of battery electric vehicles. Electric vehicle sales are expected to grow significantly over the coming several decades, supported by extensive Government policy actions, point-of-sale incentives, development of charging infrastructure networks, developing consumer preferences, and decreasing costs with manufacturing scale and technological advancements.

Global EV Sales (Millions)

Lithium-ion Battery Capacity (GWh)

Source: Benchmark Minerals Intelligence Q3 2023, Flake Graphite Forecast

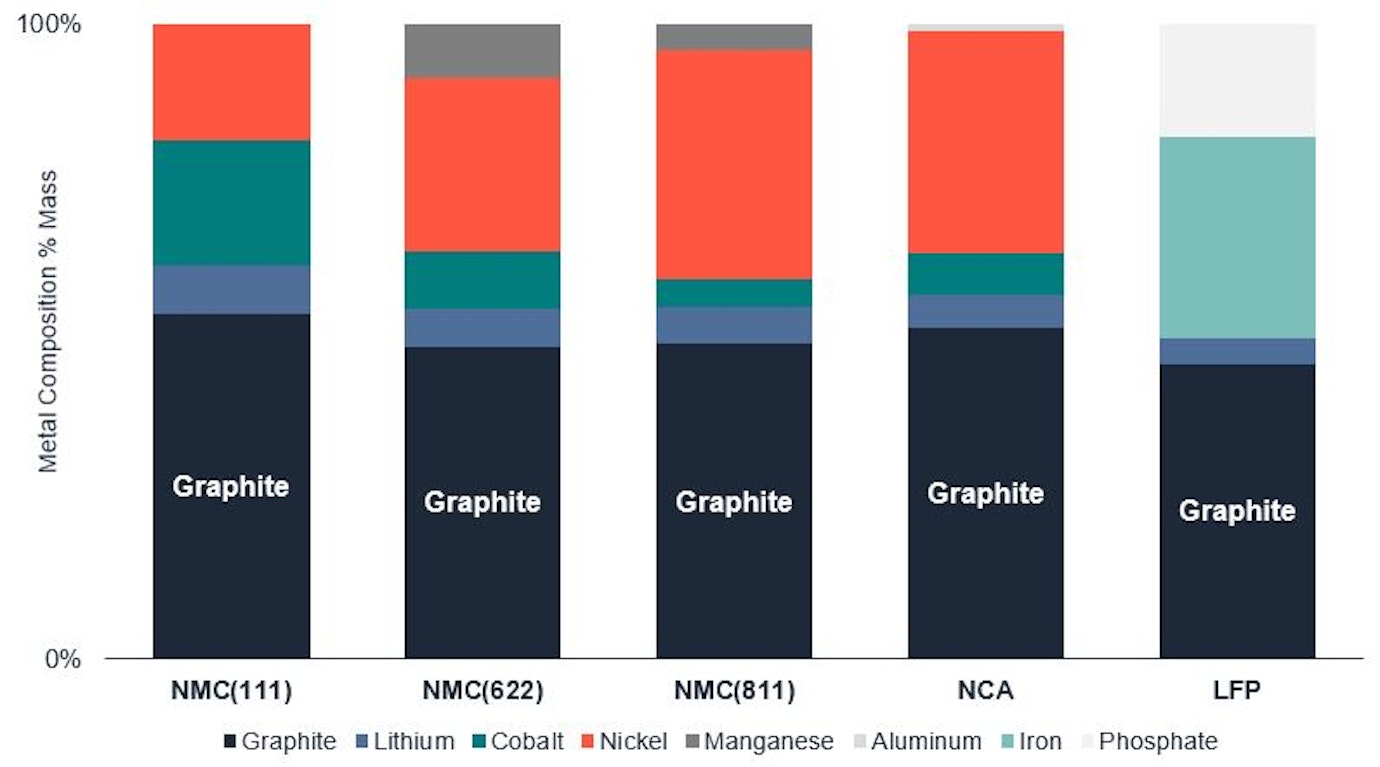

Battery Anode Composition

Graphite is the dominant input material in active anode materials for lithium-ion batteries across all cathode chemistries, including high nickel content (NCM and NCA) and lithium iron phosphate (LFP) batteries.

Raw Materials Composition of Batteries

Source: Syrah analysis, data from Gaines, L., Richa, K., & Spangenberger, J. (2018) Key issues for Li-ion battery recycling (excludes oxygen). Note 1: Percent of the total sum by elemental mass featured in the analysis for each battery chemistry, excludes oxygen (cathode).

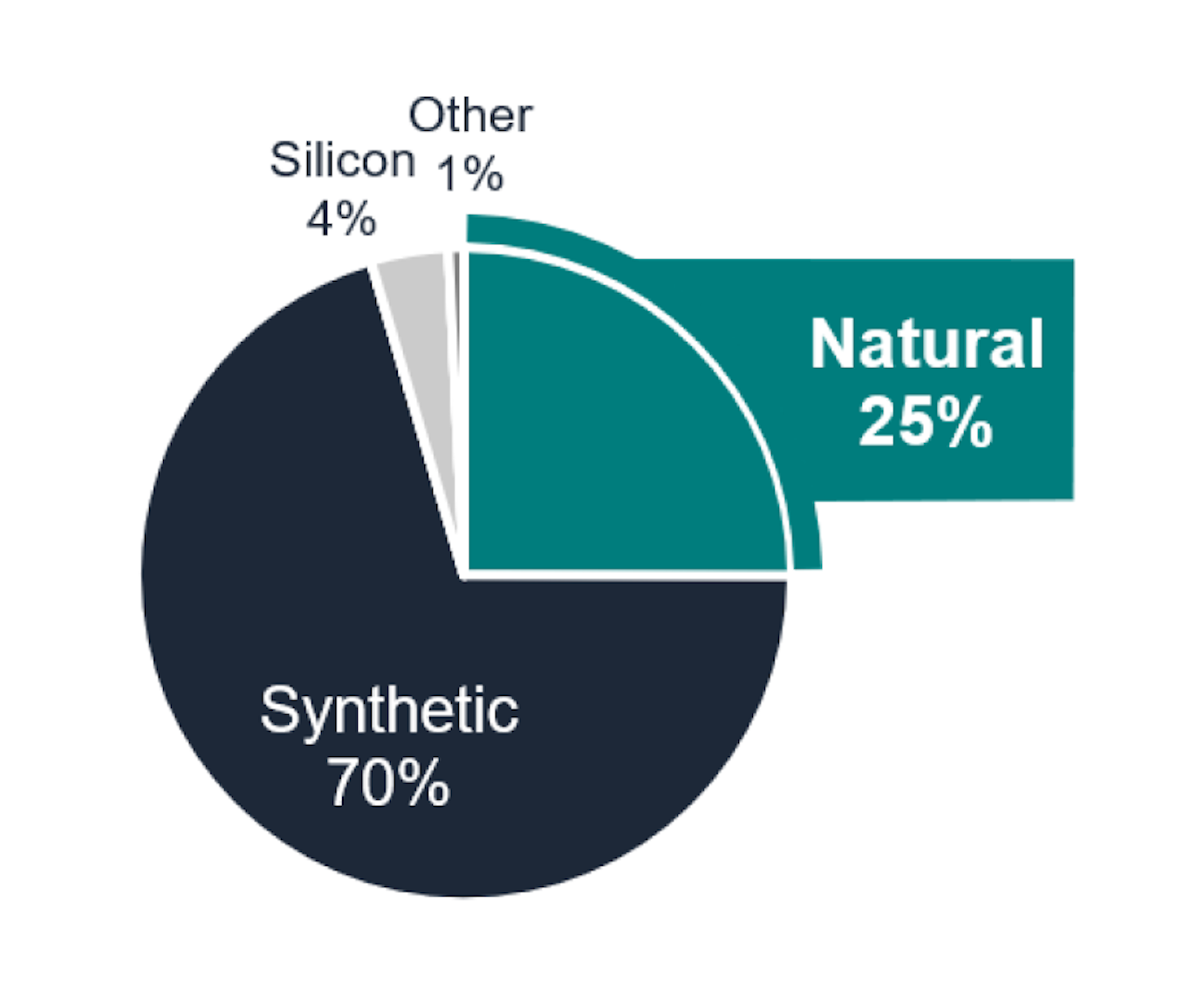

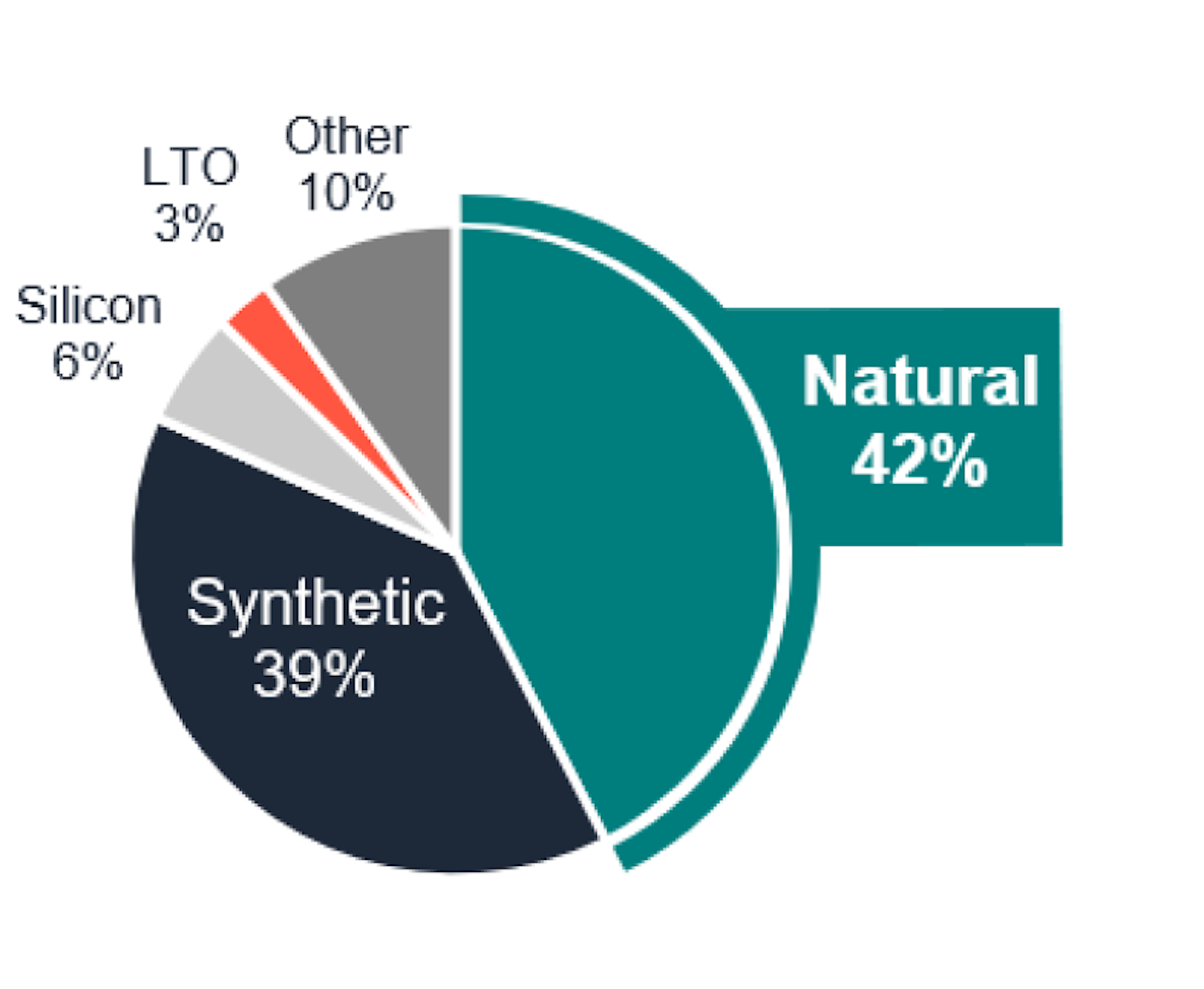

Natural graphite active anode material can be produced at lower cost and with reduced environmental impacts, and can achieve a higher capacity, compared to synthetic graphite-based active anode material alternatives. With these desirable attributes, the share of natural graphite active anode material consumed in battery anodes is forecast to increase to above 40% by mass by 2040.

2023 Composition of Active Anode Material for Batteries

2040 Composition of Active Anode Material for Batteries

Source: Benchmark Minerals Intelligence Flake Graphite Forecast, Q3 2023.

Alternative Active Anode Materials and Battery Cell Technology

Silicon is considered a potential future alternative to graphite as an active anode material. Silicon has a higher theoretical energy and volumetric density compared with graphite, translating to higher capacity, and may allow for faster charging. Silicon is currently used in small proportions of up to 5% by mass with graphite in battery anodes to take advantage of these benefits. However, silicon swells significantly more than graphite in charge/discharge cycling, causing cell instability, capacity degradation and reduced cycle life when it is used in more significant proportions in a battery anode. Technological solutions have not yet addressed these critical issues for real world application of silicon as a direct substitute for graphite at scale. It is expected that graphite and silicon will continue to be blended in future anode product development.

Even though novel battery anode and battery cell technology (e.g. solid state) are being evaluated, there are myriad technical, manufacturing and market challenges to overcome for these technologies to be commercialised and scaled in a meaningful way in the electric vehicle market. Significant base-load capacity investment has been made and is expected to continue for battery manufacturing facilities that primarily utilise graphite active anode materials in the battery anode, and these large scale, low cost facilities are largely incompatible with novel battery cell technologies.

Graphite is expected to remain the preferred and most widely used active anode material for mass market batteries, particularly for electric vehicles and stationary storage applications.

Principal Address

Level 7, 477 Collins Street

Melbourne VIC 3000

Australia